Navigating the world of health insurance can be overwhelming, especially with the plethora of jargon and terminology used in policies and discussions. Understanding these terms is crucial for making informed decisions about your health care and finances. This article will explain some of the most common health insurance terms, helping you demystify the complexities of health coverage.

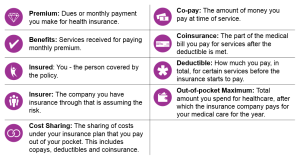

1. Premium

1. Premium

The premium is the amount you pay for your health insurance plan, typically on a monthly basis. This fee is required to keep your policy active. Premiums can vary based on factors like your age, location, the type of plan you choose, and whether you receive any subsidies. It’s important to remember that while a lower premium might seem appealing, it may come with higher out-of-pocket costs.

2. Deductible

The deductible is the amount you must pay out-of-pocket for covered health care services before your insurance begins to pay. For example, if you have a deductible of $1,000, you will need to pay that amount for services such as hospital visits or surgeries before your insurer starts to cover costs. Deductibles can vary significantly between plans, and some preventive services may be covered before reaching your deductible.

3. Copayment (Copay)

A copayment, or copay, is a fixed amount you pay for a specific service at the time of your visit. For instance, you might pay a copay of $20 for a doctor’s visit or $10 for a prescription medication. Copays are typically lower than deductibles and are designed to share the costs of care between you and your insurer.

4. Coinsurance

Coinsurance is the percentage of costs you share with your insurance provider after you’ve met your deductible. For example, if your plan has a 20% coinsurance rate, you would pay 20% of the costs for covered services while your insurer pays 80%. Coinsurance usually applies to services that require more significant medical intervention, such as surgeries or hospital stays.

5. Out-of-Pocket Maximum

The out-of-pocket maximum is the maximum amount you will pay for covered healthcare services in a plan year. Once you reach this limit, your insurance will cover 100% of the costs for covered services for the remainder of the year. This limit is beneficial as it protects you from excessive expenses in case of major health issues.

6. Network

A network is a group of healthcare providers, including doctors, hospitals, and specialists, that have contracted with your health insurance plan to provide services at negotiated rates. There are typically three types of networks:

- In-Network: Providers who have agreements with your insurance plan, offering services at lower rates.

- Out-of-Network: Providers who do not have an agreement with your insurer. Using these providers usually results in higher costs.

- Exclusive Provider Organization (EPO): A plan that requires members to use in-network providers except in emergencies.

7. Preventive Care

Preventive care refers to services that help prevent illnesses or detect health issues early on. This includes routine check-ups, screenings, vaccinations, and counseling. Under the Affordable Care Act (ACA), many preventive services must be covered by insurance without charging a copayment or deductible when provided by in-network providers. Examples include annual physicals and mammograms.

8. Pre-existing Condition

A pre-existing condition is a health issue that existed before the start of your health insurance coverage. Historically, insurers could deny coverage or charge higher premiums based on these conditions. However, the ACA prohibits such practices, ensuring that individuals with pre-existing conditions can obtain coverage without discrimination.

9. Explanation of Benefits (EOB)

An Explanation of Benefits (EOB) is a document sent by your insurer after you receive care. It outlines the services provided, the amount billed, your insurance coverage, the amount paid by your insurer, and your remaining balance (if any). Understanding your EOB is crucial for tracking your healthcare spending and ensuring accurate billing.

10. Health Savings Account (HSA)

A Health Savings Account (HSA) is a tax-advantaged savings account that allows you to set aside money for qualified medical expenses. HSAs can only be used in conjunction with high-deductible health plans (HDHPs). Contributions to an HSA are tax-deductible, and funds can roll over from year to year, making them a valuable tool for managing healthcare costs.

11. Marketplace

The marketplace is an online platform where individuals can shop for and compare health insurance plans. Established under the ACA, the marketplace allows users to view different plans, their costs, and coverage options. Depending on your income, you may qualify for subsidies to help lower your premium costs.

12. Enrollment Period

The enrollment period is a specific timeframe during which individuals can enroll in or change their health insurance plans. Open enrollment typically occurs once a year, but special enrollment periods may be available for those who experience qualifying life events, such as marriage, birth of a child, or loss of coverage.

13. Lifetime and Annual Limits

Lifetime and annual limits refer to the maximum amount an insurance plan will pay for covered benefits over your lifetime or within a single year. The ACA prohibits annual and lifetime limits on essential health benefits, ensuring that individuals do not face financial ruin due to excessive healthcare costs.

Conclusion

Conclusion

Understanding common health insurance terms is essential for navigating your healthcare options effectively. By familiarizing yourself with these concepts, you can make informed decisions that best suit your health needs and financial situation. Whether you are selecting a new plan, managing existing coverage, or seeking care, having a grasp on these terms will empower you to advocate for your health and well-being. As the healthcare landscape continues to evolve, staying informed will help you make the most of your health insurance benefits.